- What Is a Working Capital Loan?

- Basic Eligibility Requirements for Working Capital Loans

- Financial Documentation Lenders Require

- Credit Score and History Requirements

- Collateral and Personal Guarantee Requirements

- How Different Lenders Vary Their Requirements

- Common Mistakes That Cause Application Rejection

Most business owners realize they need extra cash flow at the worst possible moment—when invoices are piling up, vendors want payment, and the next customer payment won’t arrive for three weeks. You’re not alone in this situation. Roughly 82% of small businesses experience cash flow problems at some point, and working capital loans exist specifically to solve this problem.

Here’s what catches people off guard: getting approved isn’t just about having a profitable business. I’ve seen thriving companies with six-figure monthly revenues get rejected because they didn’t know lenders check seventeen different criteria before saying yes. Meanwhile, smaller operations with lower revenue sometimes sail through approval because they prepared the right documentation.

The qualification process varies wildly depending on where you apply. A regional bank might want two years of tax returns and collateral. An online platform might approve you in 48 hours based on six months of bank statements. Alternative lenders? They have their own playbook entirely.

You’ll walk away from this guide knowing exactly which documents to gather, what minimum thresholds you need to hit, and which lender types match your current business situation. No fluff—just the specific requirements that determine whether you get approved or rejected.

What Is a Working Capital Loan?

Think of working capital financing as the money covering your everyday business survival. You’re not buying a building or a delivery truck. Instead, you’re funding the gap between when you pay your bills and when customers pay you.

Here’s how it differs from other business financing: Term loans fund specific purchases like equipment. Commercial mortgages buy property. Working capital loans keep the lights on and inventory stocked. The money might cover payroll for two months while you wait on a big client payment, or it could stock your shelves before holiday shopping season hits.

These loans typically run between three months and 24 months, though you’ll find outliers on both ends. What really matters for the working capital loan requirements explained in this guide is how lenders evaluate risk differently than they do for expansion capital. They’re not asking “can this business grow?” They’re asking “does this business generate enough daily cash to repay us while staying operational?”

You’ll encounter two main structures: lump sum deposits or revolving credit lines. Get a lump sum and you receive $50,000 (or whatever amount) in one shot, then make regular payments until it’s gone. Choose a credit line and you can withdraw funds as needed up to your limit—like a credit card for your business. The structure you pick actually changes which documents lenders scrutinize most carefully during evaluation.

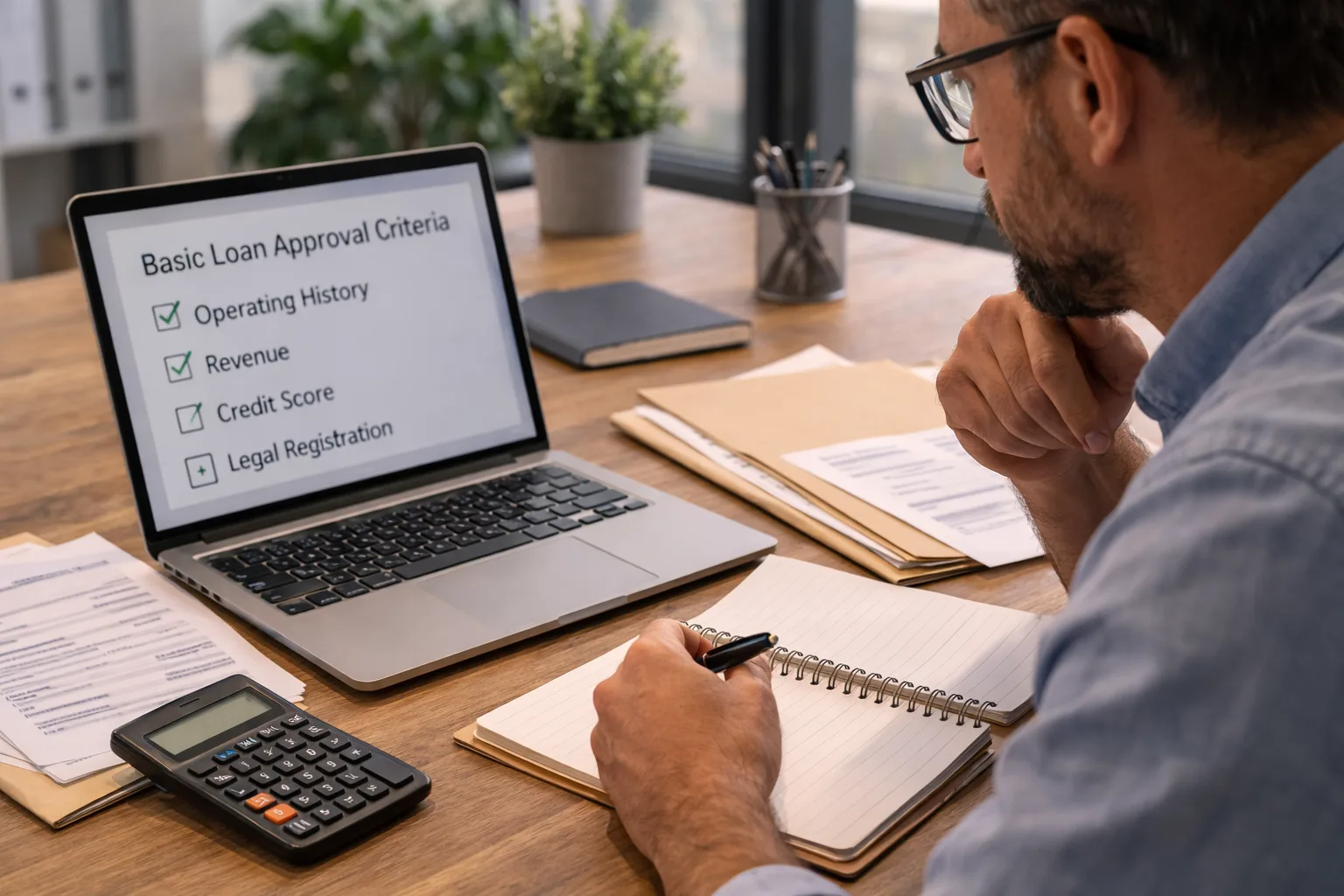

Basic Eligibility Requirements for Working Capital Loans

Let’s cut through the confusion: certain baseline standards act as immediate filters before lenders even look at your application details. Miss one of these working capital loan requirements and your application stops cold, regardless of how impressive your revenue looks.

Operating History: Six months minimum with most online lenders. Banks want two years, sometimes three if you’re requesting six figures without collateral. Started your business four months ago? Your options shrink to SBA microloans or tapping personal resources. The calendar matters more than your monthly sales at this stage.

Revenue Floors: Here’s where it gets specific. Traditional banks often won’t talk to you below $250,000 annual revenue. Online lenders drop that threshold to $100,000, sometimes $75,000. Some alternative lenders ignore annual revenue entirely, focusing instead on whether you’re depositing at least $12,000-$15,000 monthly.

Legal Registration: Your business must exist as a recognized legal entity registered with your state. Sole proprietorship, LLC, S-corp, C-corp, partnership—the structure matters less than having official registration documents. Some lenders refuse sole proprietorships above certain loan amounts because the liability protection concerns them.

Industry Restrictions: Cannabis businesses—even legal ones—get rejected by 90% of traditional lenders. Same goes for adult entertainment, speculative cryptocurrency ventures, and multilevel marketing operations. Restaurants and construction companies don’t face automatic rejection, but their higher failure rates mean extra scrutiny and documentation requirements.

Credit Minimums: Your personal credit score creates a hard floor around 550 for the most lenient alternative lenders. Most online platforms won’t approve anyone below 600. Banks draw their line at 680 or higher. Business credit scores matter too, especially once you’re requesting above $100,000, though many small businesses haven’t established business credit yet.

One requirement trips up more applicants than expected: active bankruptcies or unresolved IRS tax liens create automatic rejections across nearly all lenders. These must be discharged or settled before you apply, even if every other qualification looks perfect.

Financial Documentation Lenders Require

Documentation causes more application delays than any other single factor in the working capital loan requirements process. You might meet every qualification on paper, but if you can’t prove it with organized records, you’re not getting approved.

Bank Statements and Cash Flow Records

Pull together three to six months of business bank statements right now. Larger loans? Expect requests for twelve months. Lenders aren’t just confirming your deposits match what you claimed—they’re hunting for red flags.

What specifically are they checking? Overdraft fees signal poor cash management. NSF charges suggest you’re cutting it too close. Large, irregular deposits that don’t match your business model raise questions about income sources. They calculate your average daily balance and look for patterns: are deposits consistent or wildly erratic? Do you maintain a cushion or run near zero every month?

Some lenders now use automated analysis tools that scan your statements and flag concerns before a human ever reviews your application. These systems catch things like: mixing personal expenses in business accounts (that pizza delivery charge doesn’t look business-related), sudden spikes in deposits (did you inject personal money to inflate numbers?), or dramatic changes month-to-month.

Beyond statements, you need documented accounts receivable and payable records. Who owes you money? When are those payments expected? What do you owe and when? Informal tracking in a notebook won’t cut it—lenders want digital records or formal invoicing systems.

Tax Returns and Financial Statements

Two years of business tax returns are standard with traditional lenders. These verify you actually generate the revenue you’re claiming and show whether you’re profitable or bleeding money. Showed losses in both recent years? Prepare for tough questions about repayment ability.

Personal returns for any owner holding 20% or more stake come next. Lenders check your personal financial situation and total debt load across business and personal obligations. They want to know you’re not overleveraged everywhere simultaneously.

Profit and loss statements plus balance sheets round out this category. Many small businesses only create these at tax time—that’s a problem. Lenders prefer monthly or quarterly financials, especially if you’re applying in June but your latest tax return only shows data through December of the previous year.

Here’s something most business owners don’t consider: having a CPA prepare your financial statements instead of doing them yourself significantly improves your application strength. It costs money upfront but can mean lower interest rates or higher approval amounts that more than cover the accounting fees.

Business Licenses and Legal Documents

Proof of business registration comes first—articles of incorporation, your LLC operating agreement, or DBA filing. This confirms legal authorization to operate and clarifies ownership structure.

Current licenses and permits specific to your industry must be included. Running a restaurant? Include health department permits and liquor licenses if applicable. Contractor? State licensing and bonding certificates go in the package. Expired licenses tell lenders you’re not compliant with basic operational requirements.

Commercial leases, franchise agreements, and major contracts with suppliers or anchor customers help too. A three-year lease demonstrates stability. A contract guaranteeing $30,000 monthly from a Fortune 500 customer shows reliable future income. Partnership agreements clarify who owns what and how decisions get made.

Requests above $100,000 often trigger asks for business plans or financial projections. These aren’t always mandatory, but having them prepared anyway demonstrates you’re thinking beyond next month’s bills.

Credit Score and History Requirements

Credit requirements confuse people more than almost any other aspect of the working capital loan requirements guide. Both personal and business scores matter, but which one weighs heavier changes based on loan size and lender type.

Personal Credit Thresholds: For loans under $250,000, your personal score usually carries more weight than business credit. Banks draw their minimum line around 680. Online lenders might approve you at 600, though anything below 650 pushes your interest rate up substantially.

Scores between 550-600 leave you with expensive alternative lenders and merchant cash advance operations where costs can hit 40-60% effective annual rates. If you’re sitting at 580 right now, six months spent improving your score to 650 will save you thousands—possibly tens of thousands—in financing costs.

Business Credit Evaluation: Dun & Bradstreet scores run 0-100. Experian and Equifax use different scales for business credit. Here’s the catch: tons of small businesses don’t have established business credit scores at all, which isn’t an automatic disqualification but definitely limits your options.

Building business credit requires opening accounts in your business name, establishing trade lines with suppliers who report to bureaus, and maintaining consistent payment histories. This process takes six months minimum, often longer to develop genuinely strong scores.

Red Flags in Credit History: Bankruptcies, foreclosures, or tax liens from the past two years create major obstacles. Some lenders won’t touch these for three to five years after resolution. Multiple recent late payments matter more than your overall score—a 690 score with three 30-day late marks in the past year looks worse than a 680 score with clean recent history.

Lenders distinguish patterns from isolated incidents. One late payment from three years ago during a medical emergency? Not a deal-breaker. Six late payments scattered across the past eighteen months? That suggests chronic financial management problems.

Impact on Loan Terms: The gap between a 680 and 750 credit score might mean three to four percentage points in interest—that’s potentially $4,000-$6,000 on a $100,000 loan over 24 months. Higher scores also unlock larger approval amounts and reduce or eliminate collateral requirements.

Collateral and Personal Guarantee Requirements

Collateral and guarantee terms surprise applicants late in the approval process more than almost anything else. These working capital loan requirements requirements shift dramatically based on loan amount, your risk profile, and which lender type you’re dealing with.

Collateral Triggers: Banks typically want collateral once you cross $50,000, though individual institutions set their own thresholds. Online lenders more frequently offer unsecured options up to $250,000 if your credit and revenue look strong. Alternative lenders might skip traditional collateral but instead file liens against future receivables or inventory.

Collateral demands increase when you’re borrowing large amounts relative to annual revenue. Requesting a loan equal to 60% of your yearly revenue? Expect collateral requirements. Borrowing just 10%? You might qualify unsecured.

Acceptable Collateral Types: Commercial or personal real estate provides the strongest collateral position, typically supporting loans up to 80% of appraised value. Equipment, machinery, and vehicles work for certain loan types but get valued conservatively—expect to borrow 50-70% of market value at most.

Inventory and receivables serve as collateral in wholesale and manufacturing contexts, though lenders discount these heavily. Inventory might support loans at only 40-50% of value because liquidation is difficult and values fluctuate. Receivables work better, especially if your customers have strong credit.

Using personal assets—your house, investment accounts, personal vehicles—to secure business loans carries significant risk. Business failure could cost you your home. This approach usually surfaces for newer businesses lacking substantial business assets.

Personal Guarantee Reality: Most lenders require personal guarantees from anyone owning 20% or more of the business. Sign a personal guarantee and you’re personally liable if the business defaults. This means lenders can pursue your personal assets, garnish personal income, and tank your personal credit if the business can’t repay.

Limited guarantees cap your liability at specific amounts or percentages. These are rarer but worth negotiating, particularly in partnerships where multiple owners share risk.

Secured Versus Unsecured Structures: Unsecured loans skip collateral requirements but charge higher rates and impose stricter qualification standards. They work best for established businesses with excellent credit and steady revenue. Secured loans offer lower rates and larger amounts but put specific assets at risk if you default.

Some lenders offer hybrid approaches: unsecured loans with personal guarantees attached. You’re not pledging specific assets upfront, but the guarantee gives lenders legal recourse to pursue your personal property if needed. This simplifies applications while still providing lenders downside protection.

How Different Lenders Vary Their Requirements

Working capital loan requirements examples vary so dramatically across lender categories that you’re essentially dealing with different products entirely. Understanding these variations helps you target applications where you actually have approval chances.

Traditional Banks: National and regional banks deliver the lowest interest rates—sometimes 6-9% for well-qualified borrowers—but enforce the strictest standards. They want two or more years operating, credit scores above 680, and annual revenue that’s substantial for your industry. Applications take weeks or months, requiring extensive documentation and multiple review layers.

Banks work beautifully if you meet their standards, offering larger amounts and longer repayment periods. But their rigid underwriting provides zero flexibility for businesses with credit issues or unusual circumstances.

Online Lenders: These platforms streamline everything, often making decisions within 24-72 hours. They’ll work with credit scores down to 600 and businesses operational for just 6-12 months. The tradeoff? Interest rates run higher—commonly 12-30%—and loan amounts may be capped lower than traditional banks.

Many online lenders use automated systems that connect directly to your bank account, analyzing months of transaction data instead of requiring you to submit stacks of documents. This speed appeals to businesses needing fast cash, though the cost premium can be steep.

Credit Unions: Business credit unions sit between banks and online lenders on most factors. More flexible underwriting than banks, more reasonable rates than many online lenders. However, you must qualify for membership first, usually through location, industry association ties, or employer connections.

Credit unions take a relationship approach, sometimes considering factors beyond pure numbers. Strong existing relationships through other accounts can tip marginal applications toward approval.

Alternative Lenders: This broad category includes merchant cash advance companies, invoice factoring operations, and other non-traditional sources. They work with the highest-risk borrowers—businesses banks won’t touch—but costs can reach 40-80% effective annual rates.

Alternative lenders focus heavily on very recent performance, sometimes approving loans based solely on the past three months of deposits. They’re truly last-resort options for businesses that can’t qualify anywhere else.

| Lender Type | Credit Score Floor | Operating History | Annual Revenue Floor | Decision Timeline | Collateral Approach |

|---|---|---|---|---|---|

| Traditional Banks | 680 or higher | 24+ months | $250,000+ | 2-8 weeks | Required above $50K typically |

| Online Lenders | 600-650 range | 6-12 months | $100,000+ | 1-5 days | Often waived to $250K |

| Credit Unions | 650-680 range | 12-24 months | $150,000+ | 1-4 weeks | Depends on amount |

| Alternative Lenders | 550+ acceptable | 3-6 months | $50,000+ | 1-3 days | Lien on receivables/inventory |

These represent typical patterns in 2026, but individual lenders within each category vary significantly. Some online lenders maintain bank-like standards. Certain banks have fast-track programs for exceptional borrowers.

Common Mistakes That Cause Application Rejection

Understanding the working capital loan requirements process includes recognizing what derails applications. Many rejections stem from easily avoidable mistakes rather than fundamental disqualification issues.

Blending Personal and Business Finances: Paying for groceries from your business account or depositing birthday gift money into business accounts creates chaos during underwriting. Lenders can’t assess true business performance when everything’s mixed together. This hits sole proprietors and small LLCs hardest.

Clean separation for at least six months before applying makes a huge difference. Already mixed everything historically? Prepare detailed documentation showing which transactions are actually business-related.

Premature Applications: Excitement about a new venture leads entrepreneurs to seek financing before they’ve established sufficient history. Four months into operations? You’re too new for traditional working capital loans regardless of how well those first months went.

Wait until you legitimately meet minimum operating requirements for your target lender category. Use that time building business credit, establishing banking relationships, and creating organized financial records.

Wrong Loan Amount Requests: Asking for too much makes lenders question your judgment and repayment capacity. Requesting too little might not actually solve your cash flow problem, forcing you to reapply soon (damaging your credit through multiple inquiries).

Calculate actual working capital needs: current assets minus current liabilities equals working capital. Negative number? You need enough to bring it positive plus a buffer for ongoing operations.

Inconsistent or Missing Documentation: Revenue figures that don’t match across documents trigger immediate red flags. Bank statements missing months, tax returns without required schedules, or financial statements using different accounting methods all create problems.

Cross-check everything before submitting. Revenue on tax returns should reconcile with P&L statements and bank deposits. Discrepancies? Prepare explanations upfront.

Ignoring Debt-to-Income Calculations: Lenders calculate existing debt loads relative to income. Too much current debt makes new loans too risky. This includes business loans, credit lines, equipment financing, and sometimes personal debt for sole proprietors.

Calculate your debt service coverage ratio before applying: net operating income divided by total debt payments. Lenders generally want ratios above 1.25—meaning you earn $1.25 for every $1.00 in debt obligations.

Bad Application Timing: Applying in January or February before filing prior year’s tax returns complicates everything. Lenders want recent returns, and year-old data might not reflect current performance.

Optimal timing? Two to three months after filing annual returns, giving you recent tax documents plus several months of current-year financials showing continued strength.

Unaddressed Credit Problems: Hoping lenders won’t notice credit issues or not providing context for negative items practically guarantees rejection. Lenders see everything on your report, and unexplained problems suggest you’re either unaware or trying to hide something.

Write a brief letter addressing any credit issues directly. Explain what happened, what you did to resolve it, and why it won’t impact loan repayment. This proactive approach demonstrates responsibility.

The biggest mistake I see is business owners applying before they’re truly ready. They haven’t separated their finances, their books are disorganized, or they’re applying six months too early. Taking time to meet requirements properly doesn’t just increase approval odds—it often results in significantly better terms that save substantial money over the loan life.

Michael Chen

FAQs

Minimum thresholds range from 550 to 680 depending on where you apply. Banks generally won’t approve anyone below 680. Online lenders might work with scores as low as 600, though anything below 650 triggers significantly higher interest rates. Alternative lenders accept scores down to 550, but costs at that level often become prohibitive. Both personal and business credit matter, with personal scores carrying more weight for loans under $250,000. Scores above 720 unlock the best rates and terms across all lender types.

Six months to one year minimum with most lenders, though banks often demand two years or longer. Online lenders more commonly accept businesses operational for 6-12 months. Startups under six months face severely limited options, usually restricted to SBA microloans or personal financing sources. The longer your operating history, the more lenders you can approach and the better terms you’ll receive. Three or more years in business qualifies you for the widest range of products and most competitive rates.

Yes, but your options narrow considerably and costs increase substantially. Scores below 600 limit you mainly to alternative lenders and merchant cash advance providers, where effective interest rates commonly exceed 40-50% annually. Some online lenders approve borrowers in the 580-620 range if revenue is strong and consistent. If your score sits below 650, consider spending several months improving it before applying—the interest savings almost always outweigh the delay. Every 20-30 points you add to your score can reduce interest rates by 2-4 percentage points.

It depends on the lender, loan size, and your overall qualifications. Banks usually require collateral above $50,000, while numerous online lenders provide unsecured loans up to $250,000 for well-qualified borrowers. Even when collateral isn’t required upfront, lenders typically require personal guarantees from majority owners, making you personally liable if the business defaults. Higher credit scores, longer operating histories, and stronger revenues all increase your chances of securing unsecured financing.

Minimum documentation includes: 3-6 months of business bank statements, two years of business tax returns, current profit and loss statements, balance sheets, business licenses, and proof of business registration. Most lenders also want personal tax returns for owners holding 20% or greater stakes. Banks demand more extensive documentation than online lenders, who often streamline requirements by directly accessing bank account data through secure connections. Having all documents organized before starting your application can reduce approval time by days or even weeks.

Timelines vary dramatically by lender category. Alternative lenders and certain online lenders make decisions within 24-48 hours, with money in your account within 1-3 business days. Most online lenders complete the entire process in 3-7 days. Traditional banks require 2-8 weeks for underwriting, approval committees, and funding. Credit unions typically fall between these extremes at 1-4 weeks. Timeline also depends heavily on how quickly you provide requested documentation—incomplete applications can drag on for months.

Meeting working capital loan requirements demands organization, honest self-assessment, and strategic targeting of appropriate lenders. The institutions most likely to approve your application and offer reasonable terms depend entirely on your specific situation: how long you’ve operated, your credit profile, revenue levels, and documentation quality.

Start with honest evaluation of where you stand against the requirements outlined here. Fall short in critical areas—credit score, operating history, or revenue thresholds—and consider whether waiting to strengthen your position saves money long-term. The difference between qualifying for a bank loan at 8% versus an alternative lender at 45% represents tens of thousands of dollars on a $100,000 loan over 24 months.

Gather complete documentation before starting applications. Missing paperwork delays decisions and sometimes converts potential approvals into rejections simply because you couldn’t prove what lenders needed to see. Clean financial records, separated business and personal finances, and organized statements demonstrate professionalism that lenders value highly.

Target applications strategically. Research specific lenders’ published requirements and focus on institutions whose criteria match your profile. Shotgun applications to twenty different lenders generate multiple credit inquiries that damage your score and signal desperation to subsequent lenders reviewing your file.

Rejection from one lender doesn’t mean you can’t qualify elsewhere. Different institutions have different risk tolerances, underwriting philosophies, and target customer profiles. A bank rejection might be followed immediately by an online lender approval. However, multiple rejections across various lender types suggest fundamental issues you need to address before continuing applications.

Working capital loans solve genuine cash flow problems that nearly every business faces at some point. Accessing this funding, though, requires meeting specific standards that vary considerably across the lending landscape. Understanding precisely what lenders expect, preparing accordingly, and applying strategically positions you for approval with terms that support your business rather than creating new financial strain.