A small business loan calculator shows you the real numbers behind borrowing—what you’ll pay monthly, how much interest accumulates, and what the loan actually costs from start to finish. Before you sign documents with a lender or commit to financing that new delivery truck, running calculations helps you understand whether those payments fit your budget.

Here’s what catches most business owners off guard: they know the amount they need but haven’t mapped out how interest builds over years of payments. The difference between a three-year loan and a five-year loan isn’t just lower monthly bills—it’s potentially tens of thousands more in total costs. Understanding these numbers before you borrow keeps your cash flow healthy and your business growing.

What Is a Small Business Loan Calculator

A small business loan calculator estimates your borrowing costs by taking three essential numbers—how much you need, the interest percentage, and your repayment timeline—and showing you what to expect each month plus the full cost across the entire loan.

These tools work using the same amortization math that financial institutions apply to structure repayment schedules. Every payment you make splits between reducing what you originally borrowed and covering the interest charge. During your first year of payments, interest typically consumes the larger portion, but as time progresses, more money chips away at the actual balance. This structure explains why early payoff saves you money—you eliminate future interest before it accrues.

More detailed calculators incorporate the Annual Percentage Rate, which reveals your complete borrowing expense by folding in costs beyond the basic interest—origination fees, processing charges, and administrative expenses that lenders add. When you see an advertised rate of 7.5% but the APR reads 8.8%, that gap represents additional costs. For a $150,000 loan, that difference translates to thousands of extra dollars.

Payment frequency options in advanced calculators let you explore monthly, biweekly, or weekly schedules. Switching to biweekly payments means 26 payments yearly rather than 12 monthly ones—essentially one extra monthly payment per year. This seemingly small adjustment can trim years off your repayment schedule and dramatically reduce your interest burden.

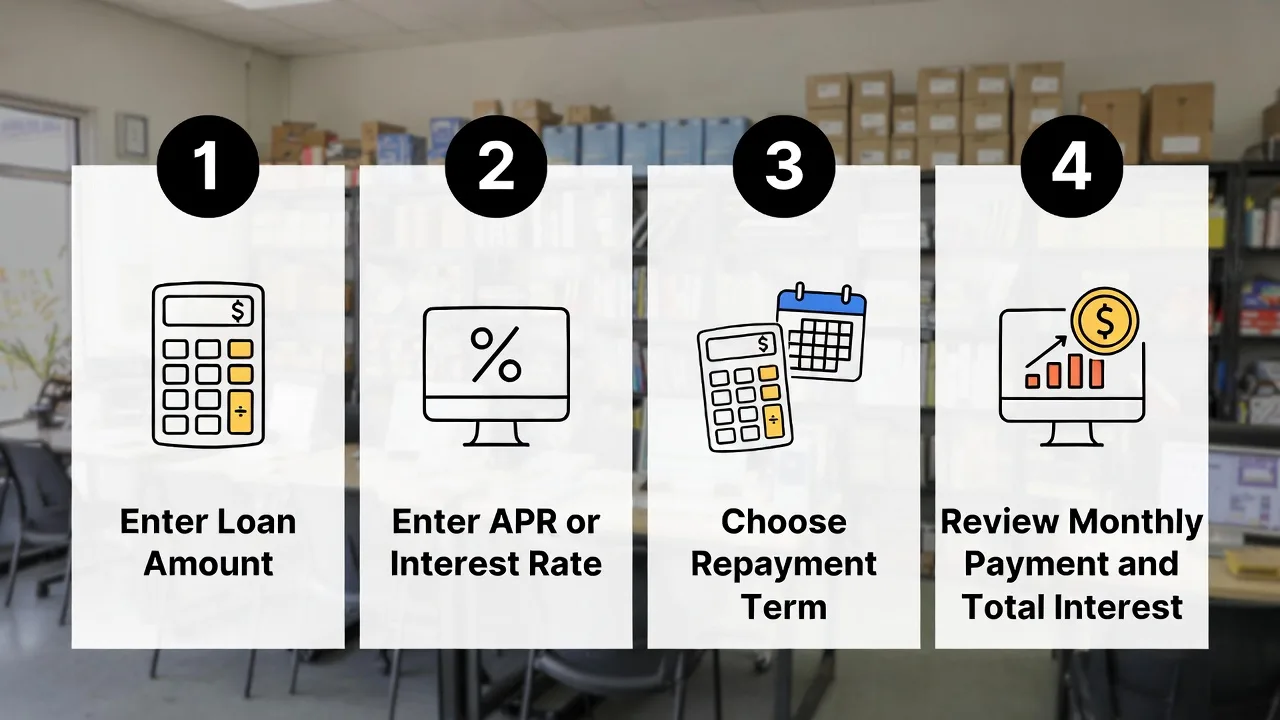

How to Use a Small Business Loan Calculator

Begin by collecting the details of your potential loan. You’ll need the borrowing amount, the interest percentage you expect based on your creditworthiness, and your intended repayment period. When you have specific offers from lenders, input the APR rather than the basic interest rate to capture the true cost.

Launch the calculator and locate the principal field—this is where you enter your borrowing amount. Need $125,000 for a restaurant renovation? Enter 125000. Next comes the annual interest percentage. A lender quoting 11.25% means you type 11.25, not the decimal 0.1125. Choose your repayment duration, which calculators display in either months or years. A three-year commitment equals 36 months.

Hit calculate and review your results. You’ll see the recurring payment amount, cumulative interest charges across the loan’s lifetime, and the complete repayment sum. Test different scenarios by changing one element at a time—this reveals how each factor influences your total costs.

Required Information and Inputs

Effective calculator use demands specific details about both your financing needs and your company’s financial standing.

Loan amount: Calculate your precise capital requirement. Underestimating leaves you scrambling for additional funding at less favorable terms later. Overestimating means paying interest on money you don’t actually need. Build a detailed budget listing every expense—new machinery, inventory purchases, building improvements, or bridging cash flow gaps during slow seasons.

Interest rate or APR: Research current lending rates for your specific loan category if you’re still exploring options. Government-backed loans currently hover between 8% and 13% for 2026, while non-traditional lenders serving higher-risk borrowers might charge anywhere from 15% to 40%. Your credit history determines your position within these ranges. Choose APR when working with actual lender proposals that include all fees.

Loan term: Repayment periods vary based on what you’re financing. When buying equipment, lenders often limit terms to match how long that equipment remains productive—typically three to ten years. Cash flow financing might run one to three years for short-term needs. Real estate financing through government programs can stretch across 25 years. Extended periods create smaller regular payments but pile on substantially more interest.

Payment frequency: Monthly payments represent the standard for business financing, though some lenders accommodate biweekly or weekly arrangements. Align your payment schedule with how revenue flows into your business. Seasonal operations might need customized payment structures, though basic calculators won’t model these specialized arrangements.

Reading Your Calculation Results

The monthly payment figure represents the cash leaving your account each period. Cross-reference this against your revenue and operational costs. Financial experts typically suggest keeping debt payments below 15-20% of monthly income to maintain healthy operations and leave room for unexpected expenses.

Total interest reveals what borrowing actually costs you. Consider a $50,000 loan at 10% across five years—you’ll spend approximately $13,640 in interest charges, making your total repayment $63,640. That identical loan compressed into three years costs just $8,070 in interest, but demands higher recurring payments ($1,613 compared to $1,061). This balance between monthly feasibility and cumulative cost shapes most financing decisions.

The complete repayment figure shows every dollar you’ll pay back. When this total seems disproportionate to your original loan amount, you’re facing either steep interest, an extended timeline, or both factors combined. Total repayment reaching 1.5 to 2 times your borrowed amount suggests shopping for better rates or reconsidering your actual capital needs.

Advanced calculators produce amortization schedules breaking down each payment’s allocation between principal reduction and interest charges. Examine your initial payments—you’ll notice minimal principal reduction early on. These schedules highlight the value of making extra principal payments during strong cash flow periods.

What You Need Before Using a Loan Calculator

Knowing your credit position helps you enter realistic rates into calculators. Business credit operates on a 0-100 scale, unlike the 300-850 range for personal credit. Scores exceeding 75 unlock preferred rates from institutional lenders, while scores under 50 push you toward costlier alternative financing. Pull your business credit reports from the major commercial bureaus—Dun & Bradstreet, Experian Business, or Equifax Business—before running calculations.

Your personal credit history also influences business loan terms, particularly for newer companies. Lenders typically demand personal guarantees on small business financing, making your consumer FICO score relevant to underwriting decisions. Scores above 700 access favorable terms; scores dipping below 650 reduce your options or inflate your rates by several percentage points.

Document your annual revenue and operational history. Lenders evaluate these metrics to gauge risk and establish appropriate rates. A company producing $750,000 annually across five years receives markedly different terms than a six-month-old startup generating $75,000 in revenue. While calculators don’t adjust for these variables, they determine the rate you should input.

Identify what assets you can pledge as security. Secured financing (backed by property, equipment, or inventory) commands lower rates than unsecured borrowing. Calculating payments for equipment financing where the equipment itself serves as collateral might reduce your rate by 2-4 percentage points versus an unsecured working capital loan.

Compile recent financial documentation—profit and loss statements, balance sheets, and cash flow statements covering the past 12-24 months. Though you won’t enter these directly into a calculator, they inform realistic loan amounts and repayment timelines you can actually sustain. Operations with unpredictable cash flow might require extended terms to manage payments comfortably, despite the increased interest expense.

Small Business Loan Calculator Example

Consider this realistic situation: You operate a commercial cleaning business and need $80,000 to acquire equipment and bring on additional employees for a substantial new contract. Your research shows rates spanning 9% to 14% depending on lender type and your qualifications. You’re weighing repayment periods between three and seven years.

Scenario 1: $80,000 at 9% interest across five years (60 months)

– Monthly payment: $1,660

– Total interest paid: $19,611

– Total repayment: $99,611

This represents strong terms, likely from a government-backed program or a traditional bank loan supported by solid credit and collateral. The monthly obligation fits comfortably for operations generating $40,000 or more monthly, staying within the recommended 15-20% payment-to-revenue ratio.

Scenario 2: $80,000 at 9% interest across three years (36 months)

– Monthly payment: $2,548

– Total interest paid: $11,718

– Total repayment: $91,718

Identical rate, compressed timeline. You preserve $7,893 in interest but your monthly obligation jumps by $888. This approach works when your new contract generates immediate revenue covering the elevated payment. The abbreviated term also means you own your equipment outright sooner and maintain flexibility for refinancing or pursuing new opportunities.

Scenario 3: $80,000 at 14% interest across five years (60 months)

– Monthly payment: $1,861

– Total interest paid: $31,682

– Total repayment: $111,682

This mirrors alternative lender pricing for companies with credit challenges or limited operating histories. The monthly payment increases just $201 versus Scenario 1, yet you surrender an additional $12,071 to interest charges. Across five years, that represents an extra $2,414 annually—enough to fund a part-time position or invest in customer acquisition.

Scenario 4: $80,000 at 14% interest across seven years (84 months)

– Monthly payment: $1,523

– Total repayment: $127,932

– Total interest paid: $47,932

The extended timeline produces the smallest monthly payment, easing cash flow pressure but extracting a steep price. You’ll pay nearly $48,000 in interest—60% of your original borrowing amount. This option only makes financial sense when contract revenue remains uncertain or your business faces pronounced seasonal fluctuations requiring maximum payment flexibility.

Compare these scenarios directly:

| Loan Amount | Interest Rate | Repayment Period | Monthly Payment | Total Interest | Total Repayment |

|---|---|---|---|---|---|

| $80,000 | 9% | 5 years | $1,660 | $19,611 | $99,611 |

| $80,000 | 9% | 3 years | $2,548 | $11,718 | $91,718 |

| $80,000 | 14% | 5 years | $1,861 | $31,682 | $111,682 |

| $80,000 | 14% | 7 years | $1,523 | $47,932 | $127,932 |

This comparison illustrates how rate and duration interact powerfully. Securing a five-percentage-point rate reduction (14% down to 9%) saves $12,071 across five years. Shortening from five years to three years preserves $7,893 in interest at identical rates. The most expensive option costs $36,214 beyond the most affordable—capital that could fund another major business initiative.

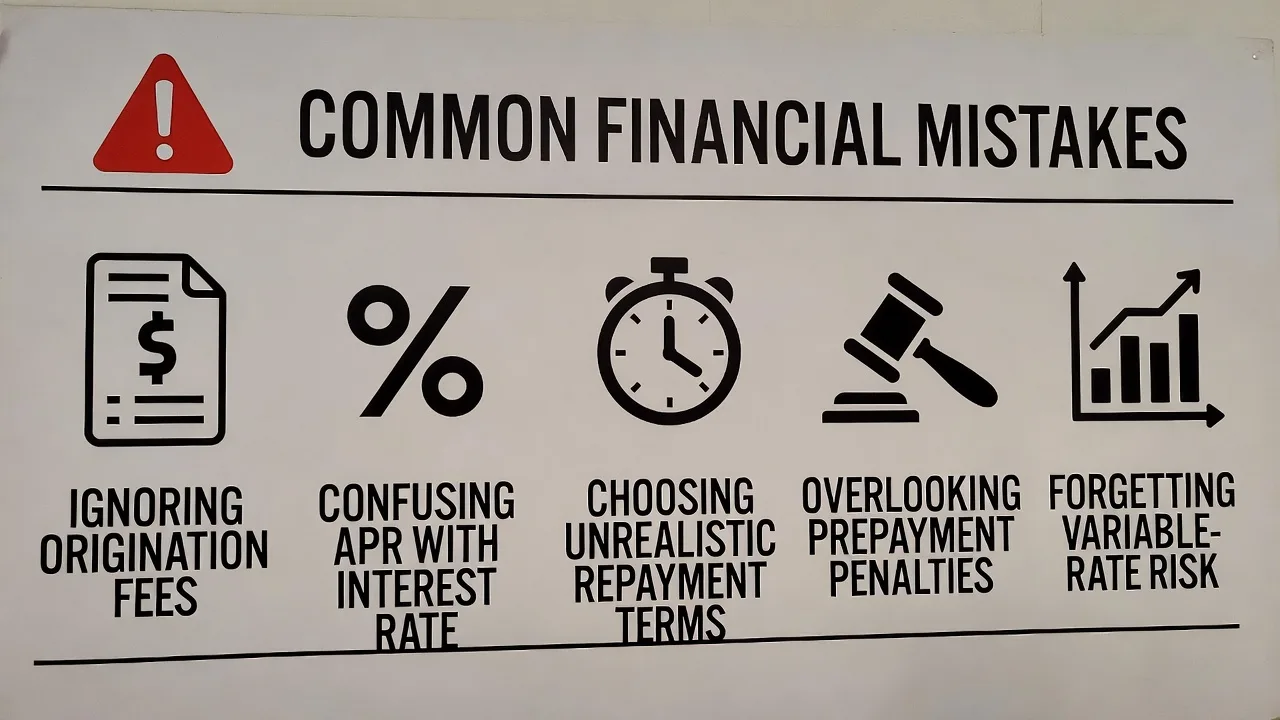

Common Mistakes When Using Loan Calculators

Business owners frequently input only the base interest percentage while overlooking origination fees, closing expenses, and other charges that lenders roll into loans. A $100,000 loan carrying a 3% origination fee delivers $97,000 to your account while requiring repayment on $100,000. Consistently use APR when available, or manually increase your principal by the fee amount to reveal actual costs.

Mixing up the base interest rate with APR produces significant calculation errors. The interest rate represents the cost of borrowing your principal amount. APR bundles that interest rate with all fees, expressed as an annual percentage. An 8% advertised rate might carry a 10% APR after incorporating a $3,000 origination charge. That two-point spread costs thousands across multi-year loans.

Selecting unrealistic repayment periods distorts your calculations. Extending to a 10-year term to shrink monthly payments looks appealing on paper, but most lenders won’t offer that duration for working capital or inventory financing. Equipment financing terms typically cap at the equipment’s productive lifespan—you can’t secure a 10-year loan for computers that become outdated in four years. Input terms that match actual lender offerings for your financing type.

Disregarding prepayment penalties creates mistaken assumptions about flexibility. Some lenders assess charges for early payoff—usually 2-5% of your remaining balance. If you anticipate refinancing or making extra payments during strong months, confirm whether penalties exist. Calculators assume penalty-free extra payments, which doesn’t reflect all loan agreements.

Overlooking variable rate structures creates planning vulnerabilities. Some business financing carries variable rates tied to benchmark rates like prime or SOFR. When these benchmarks rise, your payment increases. Calculators display fixed-rate scenarios. When considering variable-rate financing, run calculations at rates 2-3 points higher to test affordability under adverse conditions.

Misunderstanding payment frequency variations generates confusion. Converting from monthly to biweekly payments isn’t as simple as halving your monthly amount. Biweekly schedules create 26 half-payments yearly, equivalent to making 13 full monthly payments rather than 12. This accelerates payoff substantially and cuts interest costs, but calculators don’t always clearly communicate this advantage.

How Lenders Calculate Your Actual Loan Terms

Calculators deliver estimates from the numbers you input, but lenders establish your real rate and conditions through comprehensive underwriting that examines factors beyond basic calculations.

Your credit profile—both business and personal—powerfully shapes your rate. Lenders retrieve reports from multiple bureaus and scrutinize your payment patterns, credit usage, public records, and existing obligations. Two identical businesses seeking the same amount might receive rates differing by five points or more based purely on credit variations.

Revenue stability carries as much weight as total income. A business producing $600,000 annually through consistent monthly deposits appears stronger than one hitting $600,000 through irregular spikes. Lenders dissect bank statements verifying revenue patterns and evaluating your capacity for steady monthly obligations.

Operating history affects both approval likelihood and pricing. Businesses operating under two years face elevated rates or must seek alternative lenders. Reaching the three-year milestone typically unlocks improved terms, while five-plus years of operation qualifies you for the most competitive pricing—assuming other elements align favorably.

Industry and business model guide risk evaluation. Restaurants and retail operations face steeper rates than professional services firms because of higher failure statistics. Companies with predictable recurring revenue—subscriptions, contracts, retainer agreements—access better terms than project-based or seasonal operations.

Collateral quality influences secured loan pricing. Financing backed by commercial real estate receives better terms than inventory-secured loans, since inventory can depreciate rapidly. Equipment age and category matter too—new, essential equipment provides stronger collateral than older or highly specialized machinery with narrow resale markets.

Debt service coverage ratio (DSCR) measures whether your cash flow supports the new obligation. Lenders calculate net operating income divided by total debt payments. A DSCR of 1.25 or above (generating $1.25 for every dollar of debt service) typically meets approval standards. Lower ratios might trigger denial or elevated rates compensating for risk.

I see business owners concentrate on approval rather than optimal terms. Running calculations before submitting applications helps you understand what terms match your financial profile. When lender proposals significantly exceed your calculator projections, either your credit standing is weaker than expected, or you should compare offers from additional lenders.

Jennifer Martinez

Lenders also weigh your loan purpose. Financing tangible assets like equipment or property qualifies for better rates than working capital, which could fund anything. Lenders prefer seeing loan proceeds invested in revenue-generating assets rather than covering operational deficits.

Your existing relationship with a lender influences terms. Current customers maintaining deposit accounts, credit cards, or previous loans often receive rate reductions of 0.25-0.75 percentage points. This relationship pricing rewards customer loyalty and lowers the lender’s risk since they’ve already observed your payment behavior.

FAQs

Calculators deliver precise estimates based on the information you provide, but they cannot predict your actual approved terms. They employ standard amortization mathematics matching how lenders structure payments. Your real rate depends on underwriting elements including credit scores, revenue patterns, operational history, and pledged assets. Use calculators to grasp payment ranges and evaluate different scenarios, but anticipate your final loan terms varying by one to three percentage points from your estimates until you obtain formal offers.

The interest rate represents the percentage charged on your principal balance. APR bundles the interest rate with additional expenses like origination charges, closing fees, and other lender costs, all expressed as one annual percentage. An 8% interest rate combined with a 2% origination fee might produce a 9.2% APR. Always compare loans using APR because it exposes the complete borrowing cost. When a calculator only accepts interest rate inputs, manually add anticipated fees to your principal amount to approximate how APR affects your costs.

Absolutely, though you must input realistic interest rate expectations. Business credit scores under 50 or personal FICO scores below 650 typically generate rates between 18% and 40% from alternative lenders. Traditional banks often decline applications with challenged credit, directing you toward online lenders or merchant cash advance providers charging premium rates. Enter higher rates into calculators to determine whether payments remain manageable. When calculator outputs show unworkable payments even at your expected rate, consider strengthening your credit before borrowing or pursuing smaller loan amounts.

Most basic calculators don’t automatically incorporate origination fees, application charges, or closing expenses into calculations. These fees commonly range from 1% to 5% of your loan amount. To account for fees, either use a calculator accepting APR instead of simple interest rate, or add fees to your principal amount. If you need $50,000 and face a 3% origination fee ($1,500), calculate based on $51,500 to view your actual repayment obligation. Some sophisticated calculators provide separate fee fields and factor them into APR computations.

Match your repayment duration to your financing purpose and revenue predictability. Equipment financing should align with the equipment’s productive lifespan—avoid a seven-year loan for technology becoming obsolete within three years. Working capital financing typically spans one to three years since it addresses short-term requirements. Real estate financing through government programs can stretch across 25 years. Balance monthly payment affordability against cumulative interest expense. Select the shortest duration you can manage without straining cash flow, generally maintaining loan payments under 15-20% of monthly revenue.

Definitely. Calculators help you establish realistic loan amounts and comprehend true costs before investing time in applications. Execute multiple scenarios identifying your comfortable payment range, then pursue financing matching those parameters. This prevents accepting the first offer without understanding its competitiveness. Calculators also reveal whether your desired loan amount proves affordable—many business owners discover they need to borrow less or select longer terms than originally planned. Approaching lender discussions with calculated expectations helps you negotiate superior terms and identify unfavorable proposals.

A small business loan calculator converts abstract financing concepts into concrete figures you can evaluate against your operational reality. The distinction between sound financing and problematic debt often reduces to understanding these numbers before signing agreements.

Execute multiple scenarios reflecting both favorable and challenging interest rates. If you anticipate qualifying for 10% but might receive 14%, calculate both situations. The payment differential might determine whether borrowing makes sense immediately or whether strengthening your credit profile first proves wiser.

Compare cumulative interest across different durations. This comparison frequently demonstrates that extending payments across two additional years costs far more than the monthly payment reduction provides. Sometimes the financially optimal choice—an abbreviated term with elevated payments—isn’t operationally feasible given your cash flow limitations, but you’ll make that choice consciously rather than inadvertently.

Remember that calculators project ideal scenarios where everything proceeds according to plan. Build cushion into your analysis. When a calculator shows a $2,000 monthly payment consuming 18% of your revenue, that leaves minimal room for revenue declines or unexpected costs. Target loan payments representing 15% or less of your revenue to preserve financial flexibility.

Leverage calculator results to shop with confidence. When lenders present proposals, you’ll immediately recognize whether their terms reflect market rates or whether they’re embedding excessive risk premiums. This knowledge creates negotiating power and helps you sidestep predatory lending arrangements threatening your business stability.

The time you dedicate to calculating various loan scenarios generates returns throughout your entire loan duration. A few percentage points rate difference or a moderately shorter term might seem insignificant when you’re focused on securing funding, but these small variations compound into thousands of dollars over time—capital that could finance expansion, add team members, or reinforce your financial position for future opportunities.