Borrowing money quickly can mean the difference between seizing an opportunity and watching it slip away. Short-term business loans deliver fast capital, but the speed and convenience come at a price—often a significantly higher one than traditional financing. Understanding how rates work, what you’ll actually pay, and how lenders determine your pricing is essential before you sign any agreement.

What Are Short Term Business Loans?

Short-term business loans provide working capital that you repay within a compressed timeframe, typically ranging from three months to 18 months. Unlike conventional bank loans that might stretch five or seven years, these financing products prioritize speed and accessibility over long repayment horizons.

The structure varies widely. Some lenders disburse a lump sum you repay through daily or weekly automatic withdrawals. Others extend a line of credit you can draw against as needed. The unifying characteristic is the abbreviated repayment window, which directly impacts how much you’ll pay in financing costs.

Typical Loan Terms and Repayment Periods

Most short-term products fall into three categories based on duration. Loans of three to six months often target immediate cash flow gaps—covering payroll during a slow season or purchasing inventory before a major sales event. The six-to-12-month range suits moderate-scale investments like equipment repairs or small renovations. Anything extending 12 to 18 months starts overlapping with intermediate-term financing, though lenders still classify these as short-term products.

Repayment frequency matters as much as duration. Daily remittance schedules, common with merchant cash advances, can strain cash flow despite smaller individual payments. Weekly or bi-weekly schedules align better with many businesses’ revenue cycles. Monthly payments, while less common for true short-term loans, offer the most breathing room but typically require stronger credit profiles.

Common Use Cases for Short-Term Financing

Businesses turn to short-term loans when timing trumps cost considerations. A restaurant might need $30,000 to replace a walk-in freezer that failed during peak season—waiting weeks for bank approval isn’t viable. Retail shops frequently borrow to stock up before holiday shopping periods, repaying the loan from increased sales within months.

Bridge financing represents another major use case. A company might have a large contract payment arriving in 90 days but needs to cover operational expenses now. Rather than miss payroll or delay vendor payments, they bridge the gap with short-term capital. Construction contractors often use this approach between project milestones.

Emergency repairs, tax obligations, and unexpected opportunities all drive demand for quick capital. The key distinction: these loans solve immediate problems or capture time-sensitive opportunities, not finance long-term growth initiatives.

How Short Term Business Loan Rates Work

The way lenders express costs varies dramatically across short-term products, making direct comparisons difficult without understanding the underlying mechanics.

Interest Rate vs. Factor Rate Explained

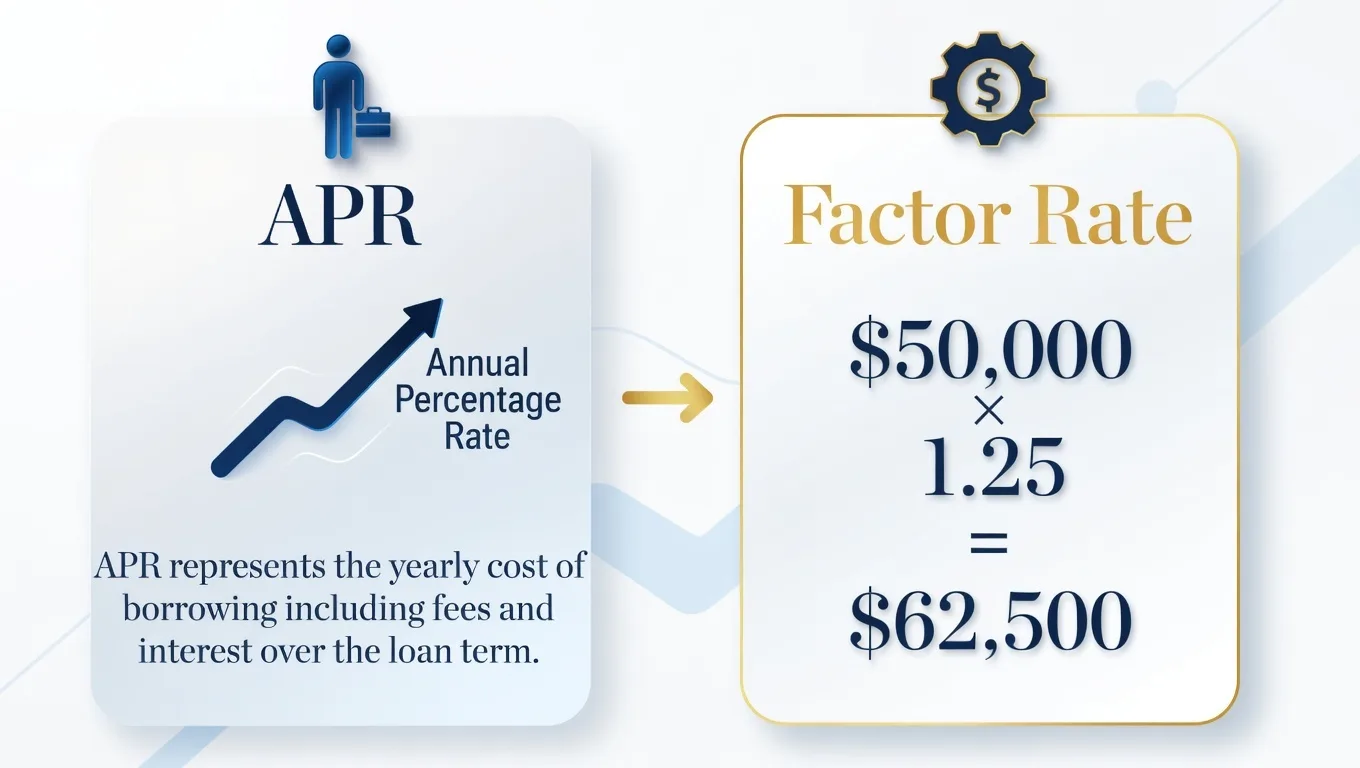

Traditional term loans quote an annual percentage rate (APR) that includes both interest and fees. You borrow $50,000 at 15% APR for one year, and the total interest cost is relatively straightforward to calculate.

Factor rates work differently and appear primarily with merchant cash advances and some alternative lenders. Instead of a percentage, you see a decimal like 1.20 or 1.35. Multiply your loan amount by the factor rate to determine total repayment. Borrow $50,000 with a 1.25 factor rate, and you’ll repay $62,500 total—a $12,500 cost.

The confusion arises because factor rates aren’t time-dependent. Whether you repay in three months or nine, the total cost remains identical. This structure means the effective APR skyrockets if you repay quickly. That 1.25 factor rate translates to roughly 80% APR if you repay in six months, but closer to 40% APR over 12 months.

Business owners often focus on approval speed and overlook rate structures entirely,” notes Jennifer Martinez, a certified financial planner specializing in small business advisory. “I’ve seen clients accept factor rate offers without realizing they’re paying triple-digit equivalent APRs. The lack of standardized disclosure across lenders creates dangerous information gaps.

Jennifer Martinez

APR vs. Total Cost of Capital

Annual percentage rate attempts to standardize comparisons by expressing all costs—interest, origination fees, processing charges—as a single annualized figure. A loan advertised at 8% interest might carry a 12% APR once you factor in a 3% origination fee.

Total cost of capital cuts through the math entirely. If you borrow $50,000 and repay $58,000, your total cost is $8,000. For short-term needs, this absolute dollar figure often matters more than the annualized rate. A 40% APR sounds astronomical, but if you’re borrowing $20,000 for four months and paying $2,400 in costs to capture a $15,000 profit opportunity, the math works.

The trap: comparing a six-month loan to a 12-month loan using only APR can mislead. The shorter loan might show a higher APR but lower total dollar cost. Always calculate both figures before deciding.

Average Rate Ranges by Lender Type

Where you borrow determines not just the rate you’ll pay but the entire experience—from application to funding to repayment structure.

| Lender Type | Rate Range | Typical Terms | Approval Speed | Min. Credit Score | Key Advantage | Main Drawback |

|---|---|---|---|---|---|---|

| Traditional Banks | 7–12% APR | 12–18 months | 2–6 weeks | 680+ | Lowest rates, established relationships | Slow approval, strict requirements |

| Online Lenders | 10–40% APR | 3–18 months | 1–5 days | 600+ | Fast funding, streamlined process | Higher rates than banks |

| Alternative Lenders (MCA/Factor Rate) | 1.15–1.50 factor (40–150% APR equivalent) | 3–12 months | 24–48 hours | 550+ | Fastest approval, minimal documentation | Highest cost, daily repayment stress |

Banks offer the lowest rates but impose stringent requirements: multiple years in business, strong credit, detailed financial statements, sometimes collateral. The application process involves relationship managers, credit committees, and extensive documentation review. For established businesses with time to spare, banks deliver the most economical financing.

Online lenders occupy the middle ground. They’ve automated much of the underwriting process, pulling bank account data and credit reports to make decisions within days. Rates run higher than banks but remain reasonable for businesses with decent credit and at least one year of operating history. The convenience and speed justify the premium for many borrowers.

Alternative lenders—merchant cash advance providers, invoice factoring companies, and specialized short-term lenders—prioritize speed and accessibility above all else. They’ll fund businesses banks won’t touch: startups, companies with credit issues, seasonal operations. The trade-off is cost. These lenders assume higher risk and charge accordingly, often structuring deals with daily repayment to minimize their exposure.

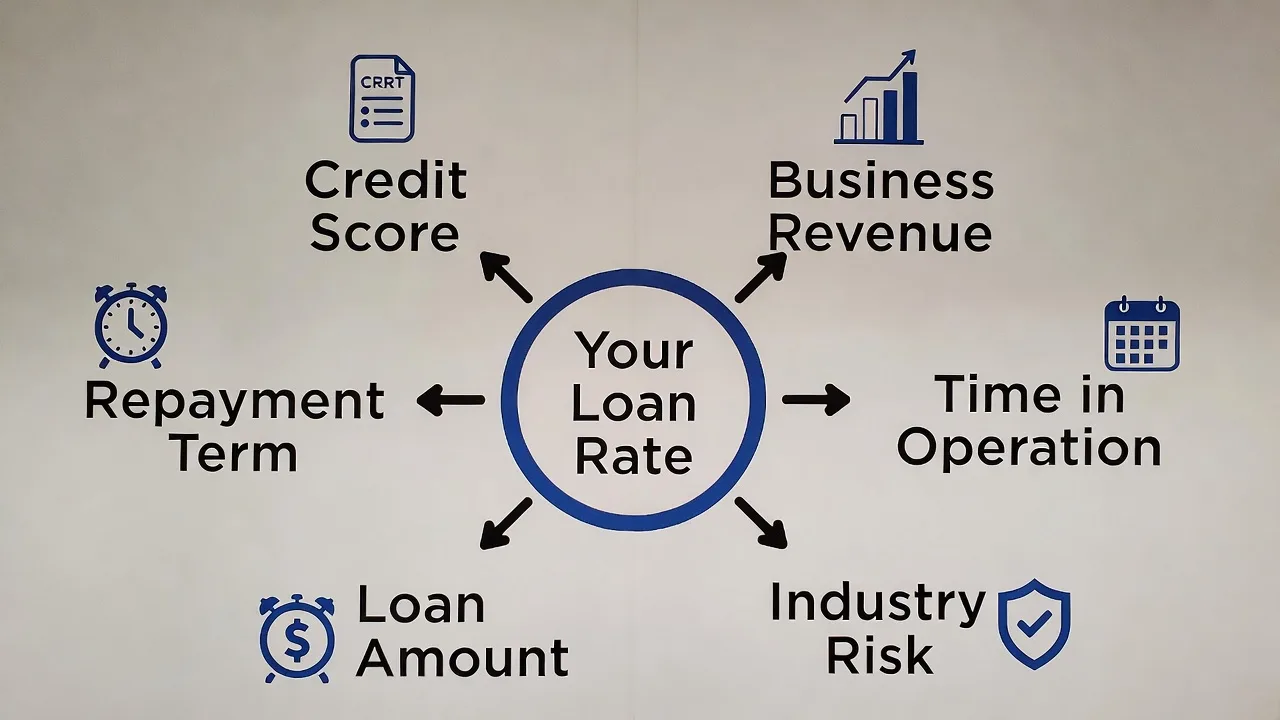

What Affects Your Rate

Lenders evaluate dozens of variables when pricing your loan, but several factors carry disproportionate weight.

Credit Score Requirements

Your personal credit score remains the single most influential factor for most lenders, especially online and bank lenders. Scores above 720 unlock the best rates—often 10–15 percentage points lower than offers extended to borrowers in the 600–650 range.

The relationship isn’t linear. Improving from 580 to 620 might drop your rate by two percentage points, while climbing from 680 to 720 could save you five points. Lenders view the 680+ range as significantly lower risk.

Business credit scores matter too, particularly for established companies. Dun & Bradstreet PAYDEX scores, Experian business credit reports, and Equifax business data all factor into sophisticated lenders’ models. A strong business credit profile can partially offset weaker personal credit, though most lenders still require personal guarantees for short-term loans.

Business Revenue and Time in Operation

Monthly revenue directly correlates with repayment capacity. A business generating $100,000 monthly can service debt a $20,000-per-month operation cannot. Most lenders set minimum revenue thresholds—commonly $10,000 to $25,000 monthly—and adjust rates based on how far above that floor you operate.

Time in business signals stability. Companies operating less than one year face the highest rates and often can’t access traditional lenders at all. The two-year mark represents an inflection point where significantly better rates become available. Businesses operating five years or more with consistent revenue receive the most favorable pricing.

Seasonal businesses face unique challenges. A ski resort with eight months of minimal revenue and four months of intense activity might show strong annual numbers but struggle with lenders who evaluate monthly cash flow. Some lenders specialize in seasonal operations and structure repayment around your revenue cycle, though usually at premium rates.

Industry Risk and Loan Amount

Lenders maintain internal risk ratings for different industries based on failure rates, volatility, and historical performance. Restaurants, construction companies, and startups typically face higher rates than established professional services firms, medical practices, or government contractors.

The spread can reach 5–10 percentage points between low-risk and high-risk industries, even with identical credit and revenue profiles. This isn’t negotiable—it’s baked into the lender’s risk models and pricing algorithms.

Loan amount creates counterintuitive pricing dynamics. Very small loans (under $10,000) often carry higher rates because the fixed costs of underwriting and servicing don’t scale down proportionally. The sweet spot for best pricing typically falls between $25,000 and $150,000. Loans exceeding $250,000 might trigger additional scrutiny and requirements that push rates up again.

How to Calculate What You’ll Actually Pay

Understanding the math behind your repayment prevents unpleasant surprises and enables accurate comparison shopping.

Start with a traditional term loan example. You borrow $50,000 at 12% APR for 12 months with a 2% origination fee ($1,000). The monthly payment is approximately $4,442. Over 12 months, you’ll repay $53,304 total—$3,304 in interest and fees combined.

Now compare that to a factor rate structure. Same $50,000 loan with a 1.25 factor rate. Total repayment: $62,500. If you repay over 12 months, monthly payments are $5,208. The effective APR is roughly 50%—more than four times the term loan rate.

The difference becomes starker with shorter repayment periods. If that factor rate loan requires repayment in six months, you’re paying the same $12,500 cost but over half the time. Monthly payments jump to $10,417, and the effective APR exceeds 100%.

Example Calculation Comparison:

| Loan Structure | Loan Amount | Rate/Factor | Term | Origination Fee | Monthly Payment | Total Repayment | Total Cost | Effective APR |

|---|---|---|---|---|---|---|---|---|

| Term Loan | $50,000 | 12% APR | 12 months | $1,000 (2%) | $4,442 | $53,304 | $3,304 | 12% |

| Factor Rate (12 mo) | $50,000 | 1.25 | 12 months | $0 | $5,208 | $62,500 | $12,500 | ~50% |

| Factor Rate (6 mo) | $50,000 | 1.25 | 6 months | $0 | $10,417 | $62,500 | $12,500 | ~100% |

Hidden fees can dramatically alter these calculations. Some lenders charge monthly maintenance fees, early repayment penalties, or processing charges that don’t appear in the advertised rate. Always request a full repayment schedule showing every fee and the total amount you’ll repay before signing.

Getting Approved and Securing Better Rates

The application process varies by lender, but preparation remains constant regardless of where you apply.

Required Documentation

Every lender requires basic identification and business verification: government-issued ID, business formation documents, and an Employer Identification Number (EIN). Beyond that, requirements diverge.

Banks demand extensive documentation: two to three years of business tax returns, personal tax returns, year-to-date profit and loss statements, balance sheets, and often accounts receivable aging reports. They’ll want to see business and personal bank statements covering at least three months, sometimes six. If you’re offering collateral, you’ll need documentation proving ownership and value.

Online lenders streamline the process considerably. Most require only three to six months of business bank statements, which they analyze using automated tools to assess cash flow and deposit consistency. Some request a profit and loss statement, but many make decisions based primarily on bank account data and credit scores. The entire application might take 30 minutes.

Alternative lenders require minimal documentation—sometimes just bank statements and identification. Merchant cash advance providers focus almost exclusively on credit card processing volume, requiring only a few months of processing statements.

Steps to Improve Your Rate Offer

If the initial rate quote disappoints, you have options before accepting or walking away.

First, address credit issues if time permits. Paying down credit card balances to reduce utilization can boost your score within weeks. Disputing errors on credit reports—which appear on roughly 20% of reports—can yield quick improvements. Even a 20-point score increase might drop your rate by one to three percentage points.

Offering collateral can significantly improve rates, especially with banks and some online lenders. Equipment, real estate, inventory, or accounts receivable provide security that reduces lender risk. The rate reduction often exceeds the risk of pledging assets, particularly if you’re confident in your ability to repay.

Shortening the loan term reduces lender risk and often improves pricing. If you requested 12 months but can manage repayment in nine, ask for a revised quote. The monthly payment increases, but the rate and total cost often decrease.

Shopping multiple lenders creates leverage. If you receive a better offer elsewhere, some lenders will match or beat it. This works best with online lenders competing for your business. Banks rarely negotiate rates, and alternative lenders have less flexibility due to their high-risk models.

Finally, consider timing. Applying when your business shows strong recent revenue—after a successful quarter or during peak season—presents a better financial picture than applying during a slow period. A few weeks’ delay might mean a significantly better rate if it allows you to demonstrate stronger cash flow.

FAQs

Context determines whether a rate is “good.” For bank loans, anything below 10% APR is excellent, 10–15% is competitive, and above 20% is expensive. Online lenders typically range 15–30%, with sub-20% rates considered favorable. For alternative lenders using factor rates, anything below 1.20 is relatively good given the speed and accessibility. Rates exceeding 1.40 (roughly 80–120% APR equivalent) should prompt serious consideration of whether the financing makes business sense.

Credit scores above 680 unlock the most competitive rates across all lender types. Scores in the 620–680 range still qualify with most online lenders but at higher rates. Below 620, you’re largely limited to alternative lenders with premium pricing. However, strong business revenue and time in operation can partially offset weaker credit. A business generating $200,000 monthly with two years of operation might secure reasonable rates despite a 640 credit score, while a startup with minimal revenue won’t qualify for competitive rates regardless of the owner’s 750 credit score.

Negotiation potential varies dramatically by lender type. Banks rarely negotiate rates—their pricing is committee-driven and based on rigid risk models. Online lenders offer limited flexibility, though presenting competing offers sometimes prompts rate matching. Alternative lenders have the most flexibility, particularly if you’re a strong candidate. Merchant cash advance providers often negotiate factor rates down by 0.05–0.10 for businesses with excellent processing volume. The key: demonstrate you’re a lower-risk borrower than their initial assessment suggested, or present competing offers that force them to sharpen their pencil.

Common additional fees include origination charges (1–5% of loan amount), processing fees ($50–$500), monthly maintenance fees ($10–$50), and early repayment penalties. Some lenders charge fees for failed ACH payments or late payments. Always request a Truth in Lending disclosure showing all fees and the total repayment amount. Reputable lenders disclose everything upfront; vague or evasive answers about fees signal potential problems. Calculate the all-in cost including every fee before comparing offers.

Short-term rates run significantly higher—often double or triple long-term loan rates. A five-year SBA loan might carry a 7–9% APR, while a six-month short-term loan from the same bank could be 12–15%. The difference reflects risk (more can go wrong over six months than five years from the lender’s perspective) and the cost structure of servicing loans. The higher rate is the price of flexibility, speed, and not tying up borrowing capacity for years. If you can qualify for long-term financing and don’t need immediate funding, it’s almost always more economical.

This depends entirely on your loan agreement. Traditional term loans with interest calculated on the outstanding balance save you money through early repayment—you pay less interest by shortening the loan term. However, some lenders charge prepayment penalties (typically 1–5% of the remaining balance) that offset these savings. Factor rate loans offer no savings from early repayment—you owe the same total amount whether you repay in three months or nine. Merchant cash advances similarly lock in the total cost regardless of repayment speed. Always clarify prepayment terms before signing, especially if there’s any chance you’ll repay early.

Short-term business loan rates reflect a fundamental trade-off between speed and cost. The fastest funding comes with the highest price tags, while the most economical options require patience and strong financial profiles. Your job isn’t finding the absolute lowest rate—it’s securing financing that solves your immediate need without creating a repayment burden that damages your business.

Before applying anywhere, calculate what you can afford to repay monthly without straining operations. Work backward from that figure to determine the maximum loan amount and acceptable rate range. Compare offers using both APR and total dollar cost, not just the advertised rate. Read every disclosure document and ask about fees until you understand exactly what you’ll repay.

The right short-term loan can bridge a critical gap, fund a growth opportunity, or solve an emergency. The wrong one—accepted hastily without understanding the true cost—can create a debt spiral that threatens your business. Treat the rate as one component of a larger decision that includes repayment structure, fees, and whether the financing genuinely makes business sense for your specific situation.