Shopping for business financing? Here’s something that’ll directly affect your wallet: the interest rate structure on your loan. You’re looking at two completely different animals here—fixed rates that never budge, and variable rates that move with the market. The difference between these two can easily mean paying $5,000 more or less over a typical loan term.

Here’s what makes this decision tricky: your brother’s restaurant might thrive with a variable rate loan while your retail shop needs the stability of fixed payments. No universal right answer exists. Your revenue patterns, how long you’ve been in business, and frankly, how well you sleep at night when payments might change—all of this matters.

How Small Business Loan Interest Rates Work

Think of interest as rent on borrowed money. You’re paying the lender for letting you use their capital instead of them investing it somewhere else. That percentage gets calculated against what you owe, turning into real dollars leaving your account each month.

Lenders size you up before quoting a rate. They’ll scrutinize your personal FICO score, dig through your business tax returns, check how long you’ve operated, and assess your industry’s risk level. A three-year-old bakery with steady revenue gets quoted differently than a six-month-old software startup burning through cash.

Now, interest rate structures come in two flavors. One camp keeps your rate cemented from day one until final payoff—we call these fixed rate arrangements. The other camp ties your rate to external benchmarks that shift monthly or quarterly as economic winds change—those are variable rate setups.

Both structures serve legitimate purposes. Fixed rates mean you can write the same check every month for years. Variable rates usually start cheaper and might save you serious money if the Federal Reserve cuts rates. Neither approach wins automatically. What fits your specific situation? That’s the million-dollar question—or at least the $200,000 question if that’s what you’re borrowing.

Traditional bank term loans lean heavily toward fixed rates. Meanwhile, business lines of credit almost always carry variable rates. Sometimes the loan product itself dictates which structure you’ll get, though more lenders now let borrowers pick their preference.

What Fixed Rate Small Business Loans Mean

Lock it in and forget it. That’s the fixed rate promise. The percentage you agree to when signing paperwork stays put whether you’re making payment three or payment sixty. Your principal-plus-interest amount remains identical month after month, making your accountant’s job infinitely easier.

This structure shields you when the Federal Reserve goes on a rate-hiking spree. Remember 2022 and 2023 when the Fed raised rates eleven times? Borrowers with fixed rates didn’t feel those increases. They kept paying their original rate while variable rate holders watched their payments climb higher each quarter.

What’s the catch? Fixed rates cost more upfront. Lenders know they’re gambling on future rate movements. If rates spike, they’re stuck collecting your lower rate while their own borrowing costs increase. That risk gets priced into your rate from day one—you’re essentially buying insurance against increases.

Flip side: you’re locked out of the upside too. When rates crater, you’re still paying that higher fixed amount unless you refinance. Refinancing means application fees, possibly $2,000-$5,000 in closing costs, fresh underwriting, and dealing with any prepayment penalties buried in your original loan documents.

Common Fixed Rate Loan Products

SBA 7(a) loans built their reputation partly on fixed rate availability. You can borrow up to $5 million with rates that don’t budge for the entire term—potentially 25 years for real estate purchases. That government backing reduces lender risk, which translates to better rates for you.

Walk into most regional banks seeking a term loan, you’re getting fixed rate terms. Whether the loan amounts to $75,000 or $750,000, banks appreciate the administrative simplicity. They underwrite once, set a payment schedule, and both parties know exactly what to expect until maturity.

Equipment financing almost universally uses fixed rates. Makes sense—you’re buying a $150,000 machine with a seven-year useful life, so your seven-year loan maintains steady payments. You can calculate true equipment costs including financing and make accurate ROI projections.

Commercial real estate loans through conventional channels typically offer fixed rates, though some include hybrid structures. The rate might hold steady for seven years, then convert to a variable structure for the remaining term. These appeal to business owners buying buildings for their operations or as investment properties.

Alternative lenders like Funding Circle and BlueVine offer fixed rate term loans running six months to five years. Yes, their rates run higher—often 12%-25% depending on your profile. But that fixed structure still provides payment certainty for businesses that traditional banks reject.

What Variable Rate Small Business Loans Mean

Your rate rides a roller coaster tied to market conditions. As external benchmarks rise or fall, your interest percentage adjusts—could be monthly, could be quarterly, depends on your loan agreement. What you pay in February might differ substantially from October if the Fed’s been active.

Why accept this uncertainty? Simple: lower entry price. Variable rates typically start 0.75% to 2% below equivalent fixed rate options. Lenders don’t need that built-in cushion against future increases because they can adjust your rate as their costs change. For a $250,000 loan, that 1.5% difference translates to roughly $3,750 less in first-year interest.

Payment unpredictability creates the real challenge. You might budget comfortably for $1,800 monthly payments, then watch that climb to $2,200 after the Fed raises rates three consecutive times. Businesses operating with slim margins or inconsistent revenue can find themselves squeezed when payments jump unexpectedly.

Here’s your safety net: rate caps. Most agreements limit single-period increases (often 2% maximum per adjustment) and lifetime increases (commonly 5-6% above your starting rate). So a loan beginning at 8% with a 6% lifetime cap maxes out at 14% no matter how crazy rates get. These caps prevent catastrophic payment shocks.

Some borrowers strategically choose variable rates planning to pay loans off quickly. Borrow $100,000 for seasonal inventory, expect to repay everything within 14 months? That lower variable rate probably saves money even if rates edge up modestly during repayment.

How Variable Rates Are Calculated

Prime Rate serves as the benchmark for most variable business loans. Right now (early 2026) Prime sits at 8.00%. This rate represents what major banks charge their strongest customers and moves in lockstep with Federal Reserve policy changes. When the Fed cuts or raises its federal funds rate, Prime typically adjusts the same day by the same amount.

Your actual rate equals Prime plus your margin (also called spread). A borrower with excellent credit, strong revenue, and solid collateral might qualify for Prime + 1.5%, currently totaling 9.5%. Someone with bruised credit and shorter operating history might face Prime + 4%, putting them at 12%.

Larger commercial loans increasingly use SOFR (Secured Overnight Financing Rate) as their foundation. SOFR tracks the cost banks pay borrowing cash overnight using Treasury securities as collateral. It replaced LIBOR back in 2023 and tends to move more gradually than Prime, though it still reflects Federal Reserve policy shifts.

Adjustment frequency significantly impacts your experience. Monthly repricing means you’ll feel every rate movement quickly—catching declines faster but also absorbing increases sooner. Annual adjustments give you twelve months of stable payments between changes. Lines of credit typically reprice monthly since you’re constantly drawing and repaying. Term loans more commonly adjust quarterly or yearly.

Watch for rate floors hiding in loan documents. A floor prevents your rate from dropping below a specified level regardless of how low benchmarks fall. An 8% floor means you never pay less than 8% even if Prime crashes to 3%. Floors protect lenders but eliminate your downside benefit if rates plummet.

Key Differences Between Variable and Fixed Rate Loans

Here’s the core trade-off: certainty versus opportunity. Fixed rates eliminate monthly payment surprises completely. Variable rates offer potential savings but demand comfort with uncertainty.

Who bears the risk? That’s the fundamental question. Fixed rate structures shift interest rate risk onto the lender—if rates climb, they absorb the lost income. Variable structures push that risk onto you—rising rates mean fatter payments and more total interest paid.

Term length dramatically affects which option makes strategic sense. Short loans of 12-36 months limit your exposure to rate volatility. Maybe rates increase one or two times during repayment—not catastrophic. Longer commitments stretching 7-10 years? You’ll almost certainly see multiple rate cycles, making fixed rate stability more valuable.

Prepayment terms vary more by lender than rate type, but fixed rate loans commonly include prepayment penalties. Why? Lenders want to collect their anticipated interest income. If you pay off a five-year fixed rate loan after eighteen months, the lender’s expected returns evaporate. Variable rate loans may allow prepayment more freely since lenders can quickly redeploy that capital at current market rates.

| Feature | Fixed Rate | Variable Rate |

|---|---|---|

| Payment consistency | Same dollar amount every single month | Changes based on benchmark rate shifts |

| Rate adjustments | Zero—locked for entire term | Reprices monthly, quarterly, or annually |

| Ideal loan duration | Longer commitments (5+ years) | Shorter terms (1-3 years) |

| Risk bearer | Lender absorbs rate increase risk | Borrower handles rate volatility |

| Current APR ranges | 7.5%-14% typical starting point | 6%-12% initial rate |

| Early payoff terms | Frequently penalized | Generally more permissive |

Want to compare total costs? You’ll need to make assumptions about future rate movements. Borrow $200,000 at fixed 9% for five years, you’re paying roughly $49,800 in interest. Start with a 7% variable rate? If rates stay flat you’ll save money. If rates jump 3-4 percentage points over those five years, you could pay thousands more.

Cash flow patterns matter enormously. A consulting practice with $40,000 monthly retainer income can absorb $500 payment increases more easily than a seasonal business that makes 60% of annual revenue in three months. Match your rate structure to your revenue reality.

Which Rate Type Should You Choose

How do you handle uncertainty? That’s question one. Conservative business owners who need exact budget numbers for planning should lean toward fixed rates. Entrepreneurs comfortable with calculated risks and confident they can handle payment fluctuations might embrace variable rate savings potential.

Current rate environment provides crucial context. We’re in a high-rate environment in early 2026, with the Federal Reserve signaling potential cuts later in the year. This scenario makes variable rates more attractive—you might capture those decreases. Conversely, when rates bottom out and the Fed hints at increases coming, locking in a fixed rate makes obvious sense.

Business maturity influences your ideal choice. Established companies with three years of profitability and $100,000+ in cash reserves can weather variable rate increases more comfortably than startups operating within $10,000 of breakeven monthly. New businesses benefit enormously from fixed rate predictability during vulnerable early years.

What are you financing? If you’re borrowing $300,000 for a specific expansion with clear ROI projections, calculate whether variable rate savings justify the risk. For working capital lines of credit you’ll tap and repay repeatedly, variable rates tied to Prime make logical sense since you only pay interest on outstanding daily balances.

Any loan representing more than 15% of a business’s monthly revenue? I’m pushing hard for fixed rates. Payment stability becomes worth that slightly higher rate because it prevents the domino effect problems when unexpected rate increases force owners into impossible choices between making loan payments and covering payroll.

Jennifer Martinez

Think about your bandwidth for financial management. Monitoring variable rates requires watching economic news, maintaining bigger cash reserves for potential payment jumps, and running scenarios about future rate movements. Busy owners focused on operations rather than finance often find fixed rates reduce cognitive load significantly.

Consider the gap between your fixed and variable options. If fixed comes in at just 0.5% higher, that peace of mind seems worth the modest cost for most borrowers. If the variable rate starts 2% lower? Now you’re looking at substantial potential savings that become hard to ignore, especially for terms under three years.

How to Qualify for Fixed or Variable Rate Loans

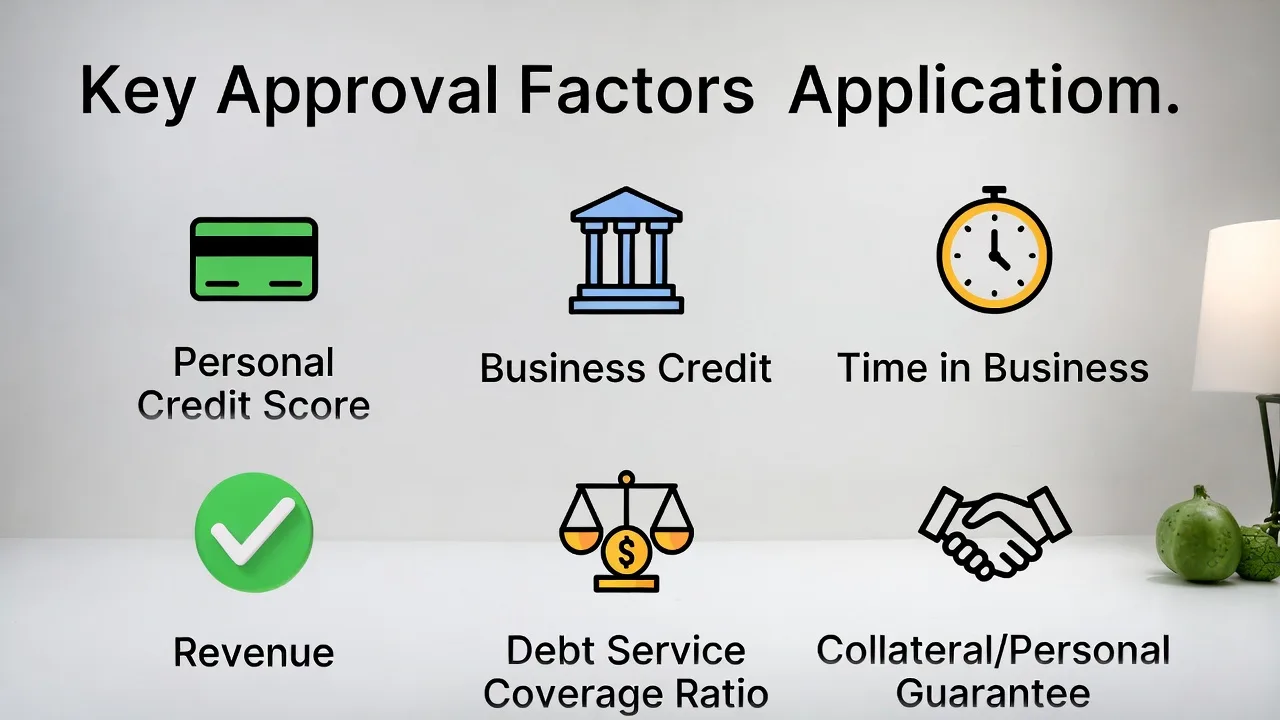

Qualification standards don’t shift based on whether you want fixed or variable rates—lenders apply identical criteria to both. They’re evaluating your personal credit profile, business credit reports, revenue trends, and debt service coverage ratio.

Most traditional lenders draw a line around 680 for personal credit scores when offering competitive rates on either structure. Scores between 640-680 remain workable but expect higher rates or requirements for additional collateral. Drop below 640? You’re looking at alternative lenders specializing in higher-risk profiles, where rates might start at 18%-25%.

Revenue documentation forms your application’s backbone. Count on providing two or three years of business tax returns, detailed profit and loss statements, and balance sheets showing your financial position. Newer businesses without extensive history may substitute personal tax returns and detailed financial projections showing how you’ll repay.

Time in business requirements vary considerably by lender and product. Traditional banks often insist on two years operating history. Online lenders might work with businesses just six months old. SBA loans require you to demonstrate exhaustion of other reasonable financing options before they’ll approve your application.

Lenders want to see your debt service coverage ratio (DSCR) hitting at least 1.25. This metric shows your operating income exceeds your total monthly debt obligations by 25%. Calculate it by dividing your annual net operating income by your annual debt payments. Higher ratios above 1.5 dramatically improve approval odds and help you negotiate better rates.

Application processes follow similar patterns regardless of rate structure. You’ll complete detailed applications, provide financial documentation, authorize credit pulls on personal and business credit, and potentially pledge collateral or personal guarantees. Traditional banks consume 30-60 days for approval and funding. Online lenders might approve and deposit funds within five to seven business days.

Collateral requirements depend far more on loan size and lender type than fixed versus variable distinctions. Secured loans backed by equipment, inventory, real estate, or accounts receivable consistently offer better rates—both fixed and variable—than unsecured term loans. That collateral directly reduces lender risk, converting to lower borrowing costs for you.

Personal guarantees accompany virtually all small business loans under $250,000. You’re pledging personal assets should the business default. This requirement applies equally whether you choose fixed or variable rates. Personal guarantees become negotiable only for larger loans exceeding $500,000 to companies with substantial operating history and assets.

Shopping multiple lenders gives you leverage and exposes options. Your current bank where you maintain business checking might offer convenient service but rarely provides the most competitive terms. Online lenders, credit unions, and alternative finance companies compete aggressively and frequently beat traditional bank pricing.

FAQs

You’ll need to refinance into a completely new loan product. This means applying fresh, going through full underwriting again, and using new loan proceeds to pay off your existing variable rate loan. Expect closing costs and fees totaling 1-3% of the loan amount—on a $200,000 loan, that’s $2,000-$6,000 upfront. Refinancing makes financial sense when your variable rate has climbed significantly above available fixed rates or when you’re confident further increases are coming. A few lenders offer rate conversion options within existing agreements, but these remain uncommon for small business loans. Run the numbers carefully: will long-term savings from switching to fixed rates justify those upfront refinancing costs?

SBA 7(a) loans come in both flavors. Fixed rate versions dominate because most borrowers prefer predictability. The SBA sets maximum rates lenders can charge based on loan size and term—generally ranging from 11-13% in the current market. SBA 504 loans, designed specifically for real estate and equipment purchases, feature fixed rates on the SBA-guaranteed portion. These loans typically involve a first position conventional loan covering 50% of costs, a second position SBA loan covering 40%, and a 10% down payment from you. Variable rate SBA loans base their rates on Prime Rate plus a negotiated margin determined by your risk profile and loan terms.

Your rate increases according to your loan agreement’s adjustment schedule—monthly, quarterly, or annually depending on terms. This directly increases your monthly payment and the total interest you’ll pay over the loan’s life. Review your loan documents for caps limiting increases. Standard caps might restrict single-period adjustments to 2% and lifetime increases to 6% above your starting rate. A loan beginning at 8% with these caps could never exceed 14% regardless of how high Prime Rate climbs. Budget defensively by maintaining cash reserves covering 3-6 months of payments at your maximum possible rate. If you started at $2,000 monthly and your capped maximum could reach $2,800, keep $8,400-$16,800 in reserves specifically for loan payment cushion.

Almost always, yes. Fixed rates typically exceed comparable variable rates by 0.5-2 percentage points at origination. Lenders build in this premium as compensation for the risk they’re accepting. They’re locked into your rate even if their own borrowing costs increase. Exact spreads fluctuate with market conditions, loan terms, and individual lender policies. In today’s environment, a well-qualified borrower might see variable rate options at 7.5% versus fixed rate alternatives at 9% for identical loan amounts and terms. Whether that higher starting rate costs more overall depends entirely on how much and how quickly variable rates increase during your repayment period. Run scenarios using different rate increase assumptions to understand your potential exposure.

Startups should strongly favor fixed rates despite higher initial costs. New businesses face overwhelming uncertainty already—adding variable loan payments into that mix creates unnecessary stress. Fixed rates provide budgeting certainty during critical early years when cash flow remains unpredictable and profit margins stay thin. Accurately forecasting monthly expenses helps startups avoid cash shortfalls that could jeopardize survival. Variable rates might work for startups with substantial financial backing, significant cash reserves (six months operating expenses minimum), or very short-term borrowing needs. A startup borrowing $50,000 for inventory expected to sell within four months might accept variable rate risk for lower costs. But for term loans extending beyond one year? Most experienced business advisors recommend startups prioritize payment stability over potential savings every time.

Your specific loan agreement determines adjustment frequency. Monthly adjustments mean your rate recalculates every 30 days based on current benchmark levels, creating frequent payment fluctuations. Quarterly adjustments strike a middle ground—you get some stability while still tracking rate trends reasonably closely. Annual adjustments provide the most short-term predictability with your rate locked for twelve months before repricing. Business lines of credit almost universally adjust monthly since you’re continuously drawing and repaying funds. Term loans more commonly use quarterly or annual adjustment schedules. Your loan documents specify the exact schedule, identify which benchmark gets used (Prime Rate or SOFR typically), and state the precise date when rates reprice. Understanding this schedule helps you anticipate when payment changes might occur and plan cash reserves accordingly.

Fixed versus variable rate decisions require honest assessment of your financial situation, comfort with uncertainty, and business stability. Fixed rates deliver payment certainty and protection when rates climb, making them perfect for longer commitments, conservative borrowers, and businesses with tight margins. Variable rates provide lower initial costs and potential savings when rates stabilize or decline, suiting shorter terms and financially flexible operations.

No objectively superior choice exists. Your specific circumstances, current economic conditions, and loan purpose and duration determine the right structure. Evaluate the rate spread between fixed and variable options, calculate worst-case scenarios for rate increases, and select the structure letting you focus on business growth rather than worrying about loan payments.

Before committing to either structure, shop at least three lenders, understand every term including caps and adjustment schedules, and calculate total costs under multiple rate scenarios. Those few hours invested in thorough comparison can save thousands of dollars and prevent significant financial stress during your repayment period.